Revue FH - 5 July 2012

In 2011, sales of wristwatches in Italy registered a significant decline compared to 2010. The figures are in fact the worst recorded since 2005, the date of the first survey.

The Italian watch magazine Clessidra has just published the results of the annual survey commissioned by l'Assorologi and carried out by GfK Retail & Technology Italia among a panel of consumers. This survey estimates sales in Italy in 2011 of 7.2 million wristwatches valued at 1.18 billion Euros. This corresponds to a downturn of 4.1% by volume and 3.5% by value compared to 2010. It should be noted that sales figures in 2011, both in volume and value terms, are the lowest recorded since 2005, the year of the first survey.

The average price rose slightly by 0.5% to 164.70 Euros. 6.2 million people, or 10.5% of the population (10.7% in 2010) made a purchase in 2011, of whom 15% bought two watches.

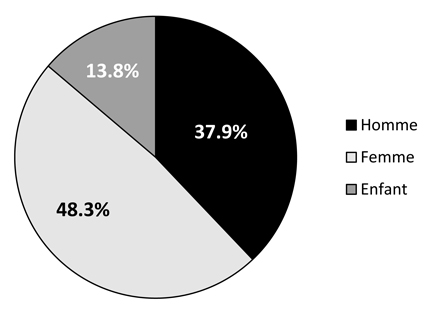

Purchases of ladies' watches accounted for 48.3% of the total by volume, compared to 37.9% for men's watches and 13.8% for children's watches. In 2010, the proportion of ladies' watches was 50.5%. In value terms, men's watches took the largest market share with 51.3%, marking a decline nonetheless in relation to 2010 (52.8%).

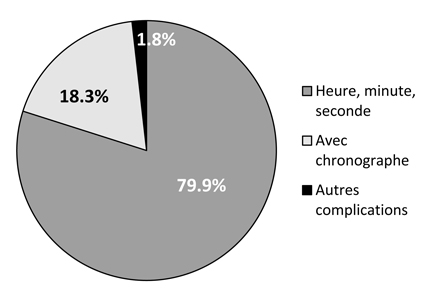

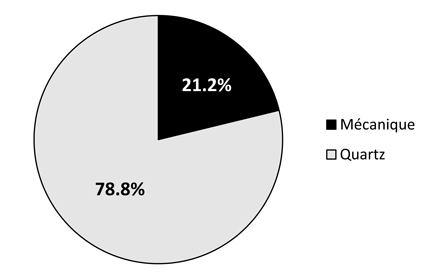

Quartz watches were in the forefront, accounting for 78.8% by volume and 57.1% by value of total sales. In 79.9% of cases, purchased watches offered only the hour/minutes/seconds function, while 20.1% were chronographs or featured other complications. As observed in the past, buyers chose predominantly steel cases (72.4% of purchases). Gold watches registered a decline with 4.9% of sales by value. Metal bracelets were favoured (41.7% of purchases by volume) over leather straps (20.9%) or plastic wristlets (31.1%).

© Revue FH

45.5% of purchases by volume and 58.1% by value were made at jeweller's stores, mainly those located in shopping centres, whose numbers are increasing every year as a result of new openings. Single-brand stores (8.3% by volume, 9.3% by value) also showed an increase, whereas supermarkets declined in importance (3.4% by volume, 1% by value). Sports shops (2.2% by volume) and fashion outlets (2.1%) were more marginal. Online sales were up and accounted for 4.9% of purchases by volume and 2.9% by value. Other distribution channels (street stalls, telephone sales, children's shops, etc) accounted for 17% by volume and only 6.5% by value.

The survey indicates that 39.2% of purchases are not associated with a particular event: 19.8% were bought for a birthday or anniversary, 19.4% for Christmas and 7.4% for communions. Saint Valentine's Day had no major bearing on watch sales (only 0.9%), even though producers increase their promotional activities during this period. It is surprising to note that for many people, the purchase of a watch is an impulse buy. In 34.7% of cases, the decision to buy is made the same day. However these figures are in decline compared to 2010, which implies that the crisis is causing consumers to reflect more before making a purchase.

58% of products were bought as a gift for another person and in 54.6% of cases the recipient was a woman. For the latter, the most important age group is between 30 and 40.

Knowledge of the product was acquired for the most part at the point of sale or from different types of watch advertising. Among those surveyed, the decision to make a purchase was strongly linked to the design of the watch (35.8%), knowledge of the brand (18.4%) and price (16.8%)